Tanya Pronina

My activities envisaged the involvement in a sound management of chemicals at the national level. My professional interests are dedicated to health and environment.

Around the world, in order to protect health and the environment, countries need to set in place and enforce effective national legislation, regulations and/or standards regarding chemicals of concern. The documents on this page are intended to help governments and industries create laws or adopt standards to limit the production, import, sale, and use of chemicals of concern.

My activities envisaged the involvement in a sound management of chemicals at the national level. My professional interests are dedicated to health and environment.

As we strive towards a better world, we work to ensure chemistry’s contributions are realized. Chemistry can help us to understand, monitor, protect and improve the environment around us.

LEEP is an international NGO working to reduce childhood lead poisoning.

I obtained MSc in Environmental Science and Management from Haramaya University.

Angela Pinilla works in the interface of science, business strategy, and safer chemicals.

Program Officer – ADEME—French environmental agency Responsible of Extended Producer Responsibility. (EPR) program for chemical products Supervise and monitor EPR program performances Recommend strategy and advise the competent authorities (MoE).

We are in the midst of a triple planetary crisis. Climate change, biodiversity loss, and pollution endanger the environment and all Earth’s inhabitants – including us. Five of the nine planetary boundaries have been crossed, creating an environment beyond the safe operating space for humanity. Each of the problems, from rising rates of extinction to carbon emissions and plastic pollution, is drastic and frightening on its own. They also interact.

Given the rates of environmental decline, the interactions between climate change and chemical pollution are especially pernicious. The chemical sector is part of the climate problem because of its own greenhouse gas (GHG) emissions and the global warming potential (GWP) of some of the chemicals it produces. Yet, through green chemistry, it could be part of the solution. The need for such solutions is urgent. A warmer world, with less predictable weather patterns and more intense storms, alters how chemicals behave in the environment and how we are exposed to them.

There are dangerous feedback loops. Climate change can lead to shifts in chemical production and use, which, in turn, could fuel further climate change. Some of these links are relatively direct. A warmer world increases the demand for air conditioning. This requires chemical refrigerants. More demand boosts production and, consequently, emissions from the sector. Other feedback loops could be less obvious. There will be more droughts and flooding, which could increase pest and disease outbreaks. This could lead to further use of pesticides and fertilizers. Again, there is an increase in demand and emissions, which adds to the climate crisis.

There is growing evidence of the many varied interconnections between climate change and chemical production and use. Yet, governance of these issues is largely working in silos. Climate change actors deal with reducing emissions and adapting to a warmer world but largely ignore chemicals. Chemicals actors are slowly drawing links to climate change (with the exception of the ozone regime that holds global warming as a central issue). This Policy Brief considers the interactions between climate change and chemicals in more detail, maps the governance connections – or lack thereof, and considers options for the future.

Chemicals are a climate problem

The chemicals sector both produces GHGs on its own and contributes significantly to the global demand for fossil fuels. The chemical sector is the third largest industrial emitter of carbon dioxide (CO2). According to the Intergovernmental Panel on Climate Change (IPCC), the chemicals sector was responsible for 14% of industrial GHG emissions in 2019 (see Figure 1). It is also the single biggest industrial user of fossil fuels for both energy and feedstock purposes. Natural gas, followed by coal, are widely used energy feedstocks.

Figure 1. Global GHG emission trends by industry subsectors

Source: IPCC Working Group III Summary for Policymakers

During chemicals manufacture, GHG emissions come from fossil fuel combustion, electricity use, and fossil fuels used as chemical feedstocks. GHG emissions are also by-products of chemical reactions. About quarter of emissions are industrial process emissions, and the rest are from fuel combustion. The highest share of emissions is from ammonia production, followed by high-value chemicals (e.g., ethylene, propylene, benzene, toluene, and mixed xylenes) and methanol. A recent study found that the production of “forever chemicals” (formally per- and poly-fluoroalkyl substances, or PFAS) is associated with substantial hydrochlorofluorocarbons (specifically, HCFC-22) emissions. HCFCs are potent GHGs, far more damaging to the climate than CO2. It is also used as an intermediary in PFAS production.

In addition, some chemicals themselves contribute directly to climate change. Chemicals with high GWP trap heat in the atmosphere. Several fluorinated chemicals, often used as refrigerants, have a high GWP value. These include chlorofluorocarbons (CFCs), hydrofluorocarbons (HFCs), HCFCs, and perfluorocarbons (PFCs), each of which are magnitudes more potent than CO2. The Kigali Amendment to the Montreal Protocol sought to address HFCs, in part because they were increasingly being used to replace CFCs after they were banned under the Protocol.

Climate scientists are closely considering the chemical sector’s emissions. The International Energy Agency (IEA) finds that the chemicals sector is not on track to meet net zero. The IPCC reports that, on average, the sector’s emissions grew by over 1.5% per year between 2010 and 2019. According to the IEA, the carbon intensity of the sector, that is, how much CO2 is produced per tonne of primary chemicals, has remained stable.

There are key regional differences. Chemicals production has shifted to the Global South, bringing with it the emissions from the sector. In 2020, China was responsible for roughly 57% of global GHG emissions associated with petrochemicals, while the US and Europe accounted for 6% and 5%, respectively. In part, this variation is down to where the industry gets its energy. The more coal, for example, in the energy mix, the higher the emissions from the sector.

The chemicals sector has yet to find or implement efficiencies to decrease its CO2 intensity. As a result, increased production necessarily leads to increased emissions. Reducing carbon intensity can be a step toward addressing the sector’s emissions while still meeting demand. While efficiency can be a key solution, the issue of raw materials and feedstocks remains. Overall, we still have an complete picture. Emissions reporting is improving, but as a report from Lund University makes clear, disclosure is partial and inconsistent, and complicated by long, complex value changes.

Potential solutions

Addressing climate change emissions may become a pressing concern for the industry. Pressure from governments, coupled with changes to the global energy system, may require companies to act to reduce emissions and to find alternatives to using fossil fuels as inputs. Climate action could build long-term value. There are also economic opportunities for the industry to help itself, and others, reduce GHGs, including in the transportation and aviation sectors.

There are analyses of potential solutions that the industry can implement to reduce GHG emissions in the sector, many of which point to the opportunities for reaching net zero. Net zero, as a concept, recognizes that some sectors may be difficult to fully decarbonize. Therefore, a mix of emissions reductions and offsetting or carbon capture and storage (CCS) could realize a “balance” between emissions and removals. Some research has advocated for the use of carbon capture technologies to reduce emissions in the sector, and for using carbon from sequestered CO2, called carbon capture and utilization. Biomass could potentially replace fossil fuels as raw materials, although there would be implications for land use.

There are other solutions at hand, drawing from ideas in the chemicals community, particularly green chemistry and circular economy. Green chemistry minimizes the need for hazardous substances when designing products and production processes. It mimics nature, by using renewable and biodegradable materials. The UN Environment Programme (UNEP) has outlined ten objectives for green chemistry, including using chemistry to minimize hazards, avoiding regrettable substitutions, and green sourcing feedstocks and production processes.

Similarly, circular economy thinking can help with identifying potential impacts from a product’s design to its end of life. Tools such as lifecycle assessment can include GHGs. For example, making products more reusable and repairable will decrease demand for new products and chemicals, which will reduce emissions from the sector. Renewable inputs could be a cost effective and sustainable solution for the industry.

Climate change is a chemicals problem

The impacts of climate change complicate chemicals management in several ways. There is a growing need for the sector and governments to think about climate adaptation (that is, building resilience to a warmer, less predictable world) in the context of chemicals management. It can increase the toxicity of some chemicals and amplify their releases into the environment. At the same time, climate change raises risks for chemicals and waste management facilities to keep hazardous products away from the surrounding environment and populations.

Already, the world is more than 1.1°C warmer than the pre-industrial era. Higher temperatures can lead to an increase in the toxicity of persistent organic pollutants (POPs), air pollutants, and pesticides, including organophosphate insecticides such as chlorpyrifos. Increased temperature can influence the fate and behavior of POPs, affecting how humans are exposed to these chemicals. Ecosystems are at risk as well. Ocean acidification may influence the behavior of metals in marine sediments, as well as their toxicity, impacting ecosystems and their inhabitants on the ocean floor. For animals already at the edge of their ability to survive in a warmer world, increased chemical toxicity could be particularly harmful.

Other effects of climate change are likely to amplify the releases of chemicals, either from the environment directly, or by damaging infrastructure. Melting ice is particularly worrying. Melting glaciers on the Tibetan Plateau release PFAS. Mercury may emerge from thawing permafrost. Melting Arctic ice could lead to four-fold increase in banned POPs in Arctic waters.

Flooding, “super-storms,” and other climate-fueled events can challenge chemicals management. These events can exacerbate the risks by increasing the likelihood of spills, contamination, infrastructure damage, and altered environmental conditions. For example, the Krasny Bor hazardous waste site in Russia has previously flooded. Assessment projects have tried to identify the risks of releases into the surrounding environment. The World Health Organization (WHO) has prepared guidance for public health authorities on the types of risks associated with chemicals after cyclones and flooding. For both, it highlights an increased risk of burns, poisoning, respiratory tract injuries, and injuries to workers.

Other tools of chemical management may need to be updated. Risk assessments often involve models or data on human and animal exposure. Altering the toxicity, behavior, and movement of chemicals could require updates to models and methodologies. It may also mean governments and researchers may have to enlarge their sample populations.

There will be regional differences in how climate change affects chemicals management and human exposure. The Arctic is of particular concern. It is highly vulnerable to both climate change and chemical pollution. Melting ice, coupled with changes to precipitation, water salinity, and sea ice quality, could unlock POPs and other chemicals deposited in the region, leading to unintentional releases and movement. These climate factors are associated with POPs concentrations in multiple Arctic biota. Other regions will face their own challenges. Small island States are already experiencing the effects of sea level rise, which could increase chemical releases from waste disposal sites. Solutions to chemical management in the context of a warmer, more turbulent world will have to be tailored to regional, and perhaps local, differences.

The potential impacts of climate change on the sector are wide ranging, from operations to risk assessments. There are equally a wide range of measures that could be implemented, as outlined in a 2015 UK Climate Change Adaptation Guidance.

Governance silos

Despite all the interconnections, climate governance rarely touches on chemicals specifically, and vice versa. The Vienna Convention and Montreal Protocol on ozone depleting chemicals are an exception. These treaties, working together, regulate chemicals that damage the ozone layer, and also consider the GWP of chemicals. The Kigali Amendment to the Montreal Protocol regulates HFCs, potent GHGs.

The Paris Agreement on climate change requires countries to submit or update nationally determined contributions (NDCs) every five years. The content of these pledges is almost entirely up to countries. Developed countries are required to have an economy-wide numerical target. Developing countries are encouraged to do so. In the current set of NDCs, 115 countries’ pledges include a target for industry, of which chemicals is a part. Waste is its own sector in climate planning and reporting, widely included in NDCs.

There is a role in global climate governance for the private sector and other actors to also make pledges under the UN Framework Convention on Climate Change (UNFCCC). The Global Climate Action portal encourages and tracks the pledges of a wide range of non-state actors. The portal allows for searching for chemicals companies specifically. In total, 289 chemicals companies logged an action, 263 of which made a commitment. So far, 207 of these companies have reported on their progress toward that commitment. Many of these seem to be small and medium-sized enterprises (SMEs). Of the top 20 chemical companies in the world, 11 registered on the portal, nine have at least one commitment, and five had reported back. Less than 40% of US-based Independent Commodity Intelligence Services (ICIS) Top 100 companies have net-zero goals or align with the Science Based Targets initiative (SBTi).

In chemicals governance, there have been a growing number of reports to raise awareness of the interconnections between chemicals and climate change, but little in the way of rule making to draw firmer links. The Stockholm Convention has repeatedly explored the connections between POPs and climate change. In conjunction with the Arctic Monitoring and Assessment Programme, the Secretariat produced a report as early as 2011. Another report, co-authored with the Minamata Convention Secretariat, was published in 2022. The Persistent Organic Pollutants Review Committee (POPRC) published a report on POPs and climate change in 2013 It noted that climate change could affect some criteria that the Committee’s considers when assessing chemicals, such as toxicity and long-range environmental transport (LRET).

As yet, climate change has not been incorporated in the Committee’s work. In part, this may be due to its mandate to consider the persistence, toxicity, bioaccumulation, and LRET of a chemical based on existing information and data. Models predicting future values are not considered as part of the Committee’s reviews.

In the current negotiations for the post-2020 strategic approach to chemicals and waste, there is a target related to synergies and linkages with other policies (currently, target E6). At present, the text mentions climate change, biodiversity, and other areas such as health. There is also a target related to implementing policies to encourage production with sustainable and safer alternatives. This could include policies to facilitate the use of cleaner production technologies, or product re-use and recycling, which could indirectly help reduce GHG emissions. Realizing these targets, in whatever final, adopted form they will take, will require further drawing the links between these two governance arenas.

Bridging the gaps

The biodiversity-climate link could be instructive. It took years of work, largely on the part of the Convention on Biological Diversity (CBD) Secretariat, to forge the connections and conduct outreach to the climate community. Recently, there have been decisions in the UNFCCC and CBD that recognize these connections. Most revolve around the idea of nature-based solutions (NbS). The concept has proved useful to articulate nature-climate connections in a way that facilitates actions on both sides.

At present, the chemicals-climate link lacks such a unifying concept. Climate actors may ask, “why should we do more on chemicals, specifically? What’s the value added?” Chemicals actors could ask the same questions. A concept bridging and articulating the solutions could help provide a common frame of reference and action.

Building this bridge may require collaboration. Some Secretariats, namely the UNFCCC and the Basel, Rotterdam, and Stockholm Conventions (BRS) Secretariats, are already talking about commonalities. Wider engagement among scientific communities, activists, and states could further improve knowledge of how intertwined the climate and pollution crises are, and the implications for the future.

* * *

This document has been developed within the framework of the Global Environment Facility (GEF) project ID: 9771 on Global Best Practices on Emerging Chemical Policy Issues of Concern under the Strategic Approach to International Chemicals Management (SAICM). This project is funded by the GEF, implemented by UNEP, and executed by the SAICM Secretariat. The International Institute for Sustainable Development acknowledges the financial contribution of the GEF to the development of this policy brief.

This Policy Brief is the seventh in a series featuring cross-cutting topics relating to the sound management of chemicals and waste. It was written by Jen Allan, Earth Negotiations Bulletin (ENB) Strategic Advisor. The series editor is Elena Kosolapova, Senior Policy Advisor, Tracking Progress Program, IISD.

This study, commissioned by DG Environment for the European Commission and produced by Wood and Ramboll. The objective was to assess the use of PFASs and fluorine-free alternatives in textiles, upholstry, carpets, leather and apparel, including specific focus on volumes of use, technical function, and emissions.

Non-fluorine alternatives considered were hydrocarbons, silicones, dendrimers, polyurethane, nanomaterials, and alternative technologies. The study makes recommendations for policy, including a REACH restriction on the placing on the market and use of these products that contain any PFAS, and a listing under the Stockholm Convention. It is also recommended in the report that a restriction could be combined with voluntary industry measures and provisions in public procurement to encourage substitution of PFAS before mandatory legislation is introduced.

Safer States is an alliance of diverse environmental health organizations and coalitions from across the United States committed to building a healthier world. The website features an interactive map showing chemical-related policies, including those related to building materials. A Bill Tracker provides further detail of the action taken by individual states to regulate chemicals, covering PFAS, toxic flame retardants, heavy metals, BPA and phthalates.

The sound management of chemicals and wastes requires addressing legacy problems while looking ahead to emerging areas of concern. As management needs evolve, predictable and progressive financial support becomes fundamental. Support can help developing countries meet their treaty and non-treaty obligations, but there are numerous other benefits at local, national, and global levels.

As new challenges arise, financial support can help enable timely action. Countries can improve their regulatory capacity and comprehensive risk management. They can implement pollutant release and transfer registers. Financial support can also catalyze effective communication and national coordination, which is required across government departments and agencies in charge of health, environment, agriculture, and customs. Communication is also key for identifying and discussing risks, especially with exposed communities. Financial support can enhance action across the science-policy interface, building information and monitoring mechanisms that bolster the capacity of scientific, technical, and policy communities individually and their ability to interact for science-based policymaking. Such interactions, within government or among stakeholders more broadly, can be key to identifying emerging issues of concern and avoiding regrettable substitutions. Given the global dispersion of some chemicals, local management has global benefits.

Despite these many benefits for the environment and human health, finance remains insufficient. This brief considers realized and potential sources of funding under the three components of the integrated approach: dedicated external financing; private sector involvement; and mainstreaming chemicals and wastes management into development planning. There are applicable lessons from other multilateral funding bodies that may help realize predictable funding streams for chemicals and wastes management.

Costs of Action and Inaction

There are currently no detailed financial assessments of the costs of implementing SDG target 12.4 (achieve the environmentally sound management of chemicals and all wastes throughout their life cycle). Yet, there are indications that the needs could be significant.

The Stockholm Convention on Persistent Organic Pollutants (POPs) conducts needs assessments for each Global Environment Facility (GEF) replenishment period. For the seventh GEF replenishment period (2018-2022), parties estimated the Convention’s funding requirements at USD 4.3 billion, which rose to USD 4.9 billion for GEF-8 (2022-2026).

The Stockholm Convention’s exercise highlights challenges with assessing developing countries’ needs. The estimates only address the POPs already listed in the Convention, not new POPs added at the COPs during GEF replenishment cycles. The assessment reports also highlight the limited information available on the extent of countries’ POPs stockpiles, particularly for polychlorinated biphenyls (PCBs) and new POPs. Support for completing national implementation plans could help with accurate assessments of the scale of support required. It seems a vicious circle: finance is required to get an accurate picture of how much finance is needed.

A similarly complicated picture emerges for estimating the financial needs for the sound management of waste. The Global Wastes management Outlook (GWMO) stresses the need to consider many factors when estimating “net” costs because the capital required for disposal facilities and technologies varies, as do the revenues earned from recovery operations. For example, the GWMO estimates the costs for collection and disposal using waste to energy incineration are 60-100 USD/tonne for upper-middle income countries and 40-100 USD/tonne for lower-middle income countries (Table 5.1).

These costs are substantial, but the costs of inaction are higher. There are direct costs, such as cleaning up contaminated sites resulting from poor chemicals and wastes management. For example, the US spends USD 1 billion annually to clean up hazardous waste Superfund sites. The African Stockpiles Programme estimates USD 150-176 million is required to clean up the 50,000 tonnes of obsolete pesticides in Africa.

There are also indirect effects, which can be difficult to monitor and measure. Health effects are perhaps the most significant. As the Lancet found in 2022, pollution is responsible for one in six deaths worldwide, and toxic chemical pollution represents a growing source of pollution-related deaths. Sub-Saharan Africa shoulders health-related costs due to chemical exposure, which the UN Environment Programme’s (UNEP) Costs of Inaction report estimated in 2013 would increase significantly, by approximately USD 97 billion by 2020. In the US, the annual cost of pollution-related disease in children totals USD 76.6 billion, and of occupational diseases and injuries – USD 250 billion. The EU’s median annual cost for diseases related to endocrine-disrupting chemicals is EUR 157 billion.

There are economic losses from poor management. The Lancet argues that the economic costs of disease and deaths from pollution are substantial. Around 1% of GDP is lost from premature death and disease from “modern pollution” in China, India, and Nigeria, defined as including ambient ozone pollution, ambient particulate matter pollution, lead exposure, occupational carcinogens, occupational particulate matter, gases, and fumes. Ineffective pest management practices can increase pesticide resistance and agricultural costs. For example, in Mali, such challenges were estimated to cost over USD 8.5 million per year, for cotton alone. Supporting sound chemical and wastes management now is a strong investment that can save money in the future. The Global Chemicals Outlook II (GCO-II) estimates the benefits of action to be in the high tens of USD billions annually.

Three Components of the Integrated Approach

The UNEP Governing Council agreed to the integrated approach to long-term funding of the chemicals and wastes agenda in 2013, after a consultative process. The approach aims to increase sustainable, predictable, adequate, and accessible financing for the chemicals and wastes agenda. It was partly a response to the Quick Start Programme, which, despite its successes, raised only USD 41 million over ten years. The Programme’s experience highlighted the need for adequate and sustained finance, a broader support base that includes industry, and heightened political support for chemicals and wastes management. The integrated approach introduces a commitment to pursuing three simultaneous methods of funding chemicals management:

These three components are complementary and interlinked. Some external sources co-leverage private finance. Mainstreaming chemicals into policies can set a regulatory framework for economic instruments that can leverage private finance. Industry involvement, aligned with the polluter-pays principle, can provide finance that can strengthen mainstreaming efforts. While the integrated approach to financing has mobilized significant resources, the GCO-II stressed that it has not met the needs of developing countries and economies in transition.

Dedicated External Financing

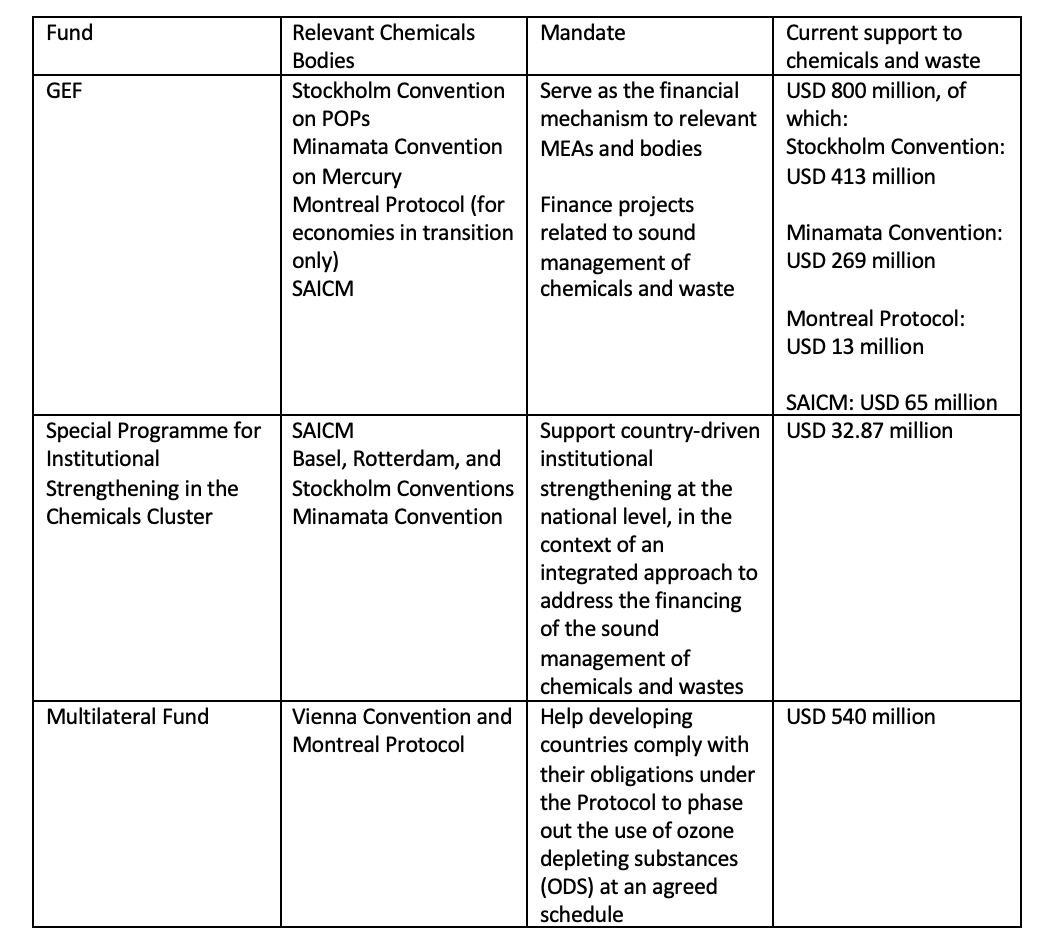

There are three multilateral funds relevant to MEAs for chemicals and wastes and/or to SAICM: the GEF; the Special Programme for Institutional Strengthening in the Chemicals Cluster; and the Multilateral Fund. For each, the scale of support falls short of the parties’ estimated needs. The table below outlines the Funds’ mandates and support they currently provide to chemicals and wastes.

GEF

GEF support for chemicals and wastes has progressively increased with each replenishment period. During the GEF-7 period, USD 599 million was allocated to the chemicals and wastes focal area. GEF-8 represents a USD 200 million increase, now sitting at USD 800 million. Overall, the chemicals and wastes focal area will receive 15% of the GEF-8 allocation, nearly matching the 16% allocated for climate change mitigation.

Over time, the GEF has moved to a more integrated approach that brings together its work to support the relevant Conventions and SAICM. During GEF-4, POPs and ODS were addressed in separate focal areas. Projects were also chemical-specific. Since GEF-5, the GEF has supported approaches that focus on sectors or supply chains. The three Conventions’ work is integrated into agricultural, industrial, and pollution control mechanisms at the national level. Projects focused on the artisanal and small-scale gold mining (ASGM) sector and the textiles supply chain include multiple chemicals and mercury. Similarly, the Implementing Sustainable Low and Non-Chemical Development in Small Island Developing States (ISLANDS) programme integrates work across the Conventions.

Special Programme

The Special Programme is different. It is a voluntary fund with a broader donor base. Governments, the private sector, and others in a position to do so are encouraged to contribute. To date, the majority of finance contributed is from governments. Eligibility criteria prioritize countries with special needs and least capacity. In 66 projects totalling over USD 17.8 million, 17 were in least developed countries and eight were in small island States.

A Midterm Evaluation found that the Special Programme is punching above its weight, meeting or exceeding its goals. However, there are concerns about sustainability of the projects, including the need for cost-recovery mechanisms or other financial assistance to continue to realize the project’s benefits.

Multilateral Fund

The Multilateral Fund supports developing countries working to meet their obligations to phase out ODS by the agreed schedules. Its replenishment cycle is two years. From 2006 to 2014, the Fund was set at USD 400 million. With the adoption of the Kigali Amendment to reduce the consumption and production of hydrofluorocarbons (HFCs), the Fund’s replenishment increased. The Amendment was adopted in 2016 and entered into force in 2019. In 2017, the Fund’s replenishment was USD 500 million and in 2022, it was increased to USD 540 million.

Mainstreaming

Mainstreaming the sound management of chemicals and wastes is the responsibility of all countries. Developing countries integrate chemicals and wastes management into their development planning. Developed countries likewise integrate these issues into international development assistance, including country assistance plans, and multilateral and bilateral agencies. Under the integrated approach, mainstreaming also involves actions that are relevant to finance such as:

National-level Mainstreaming

Communication is important to mainstreaming, according to a report synthesizing the lessons learned from mainstreaming efforts, including:

The report identifies benefits of interagency coordination, including through formalized mechanisms.

In terms of leveraging finance for chemicals and wastes management, there are a wide range of policy options available. The Organisation for Economic Co-operation and Development (OECD) suggests grants, loans, and tax exemptions are a key part of the overall policy mix for wastes management. Some examples involve direct funding, such as funding pilot projects. Others focus on the institutional conditions to finance chemicals and wastes projects, such as establishing clear liability rules under the polluter-pays principle, or a database of potentially contaminated sites. The level of investment varies across OECD states, as does the share of public finance.

International Development Finance

International development finance through the multilateral development banks (MDBs) and other channels has neglected chemicals and wastes issues. Pollution and biodiversity support in MDBs remained consistent from 1995 to 2020, while support for climate change increased. Between 2015 and 2020, household air pollution and water pollution received more attention from MDBs than ambient air pollution or chemical pollution.

While the level of attention may be consistent, there seems to be little mainstreaming in MDB decisions. The 2015 GWMO report notes that the sound wastes management represented just 0.3% of total international development finance. Of that available funding, between 2003-2012, two-thirds were allocated to ten middle-income countries. The report also notes that 70% of MDB support for sound wastes management takes the form of loans, amounting to USD 2.8 billion over the same 10 years.

Private Sector Involvement

Given the need to scale up financial resources, many have looked to industry as a source. The vision is that the private sector internalizes the costs of complying with regulations, which could include economic incentives such as taxes or subsidies. So far, as the GCO-II report stresses, “the vast majority of human health costs linked to chemicals production, consumption, and disposal are not borne by chemicals producers, nor shared down the value-chain.” It seems the aspirations of this component of the integrated approach have yet to be translated into concrete implementation.

Private Sector involvement faces several challenges:

Due to these challenges, it has proved difficult to leverage the potential of the private sector. Reviews of SAICM and the Quick Start Programme showed that private sector involvement was common, although often limited to information provision. There has been a 10% increase in private sector finance evident in SAICM progress reports between 2009-2010 and 2011-2013.

Market-based Instruments

Market-based instruments provide a price incentive for companies to act. They can complement regulatory approaches such as bans or restrictions, by creating cost-effective reasons for companies to innovate. Market-based instruments can increase the price of using a chemical. Some market-based instruments directly affect the price, such as taxes and levies. Subsidies and tradable permits are indirect methods.

The use of such mechanisms is increasing at the national level. A thematic report for GCOS II found increased use of taxes on pesticides and inorganic fertilizers, chlorinated solvents, and phthalates and brominated flame retardants. It also found increased use of refund schemes for batteries, electronic equipment, and vehicles. These measures are primarily found in high-income countries, including the use of risk-based taxation of pesticides in Denmark, Norway, France, and Mexico. Middle- and low-income countries use these tools less often.

Trading schemes allow companies to buy and sell emissions allowances on a market. For example, the costs of substituting a chemical may vary among companies, creating the opportunity to buy and sell credits. Tradeable permit systems were used in the US to phase out lead in petrol and in New Zealand to reduce nitrogen pollution from agriculture.

Overall, the use of market-based mechanisms for chemicals remains low, particularly compared to energy-related policies. There is uncertainty and a lack of data on context-specific factors, such as price elasticities, market structure, and costs of substitutes that may help set up market-based mechanisms. There is a need to study which policy instruments – regulation or markets – could be more effective for addressing different chemicals and wastes, considering different exposure effects, and substitution costs.

Extended Producer Responsibility

Extended Producer Responsibility (EPR) refers to policies that hold producers responsible for a product’s entire lifecycle. In theory, such policies can generate finance for wastes management. EPR creates incentives for producers to reduce waste generated by a product and to improve product design to ease recovery and reuse efforts. In general, EPR policies are more developed in Europe and Canada than in the US, although it varies by state. In Canada, producers pay a fee to stewardship organizations for the sound management of hazardous waste. Roughly half of US states have EPR policies.

Developing countries have significant interest in implementing EPR policies. China and India have EPR policies in place for e-waste. Following the ban on plastic bags in 2017, Kenya introduced two voluntary EPR schemes, focusing on PET plastics and bread bags (LDPE). Based on this experience, Kenya is setting up regulation for more companies to increase their responsibilities of their products, including new EPR regulations currently in development. The products subject to EPR are: packaging for hazardous and non-hazardous products, e-waste, end-of-life motor vehicles, and non-packaging items.

These efforts face additional complications. There is often a large informal sector that dismantles and recycles waste. Developing countries also receive hazardous waste from developing countries, including through illegal trade. There may be a need for a global notion of EPR, given the global trade of hazardous wastes.

The Way Forward Under the Integrated Approach

There is more work to be done under each component of the integrated approach. Financial support has so far been insufficient, prompting new ideas as countries look ahead to the new SAICM beyond 2020 framework. The African Group has proposed a globally-coordinated fee on the sale of basic chemicals and chemical feedstocks, as well as an international fund dedicated to chemicals and wastes. Iran and the International Conference of Chemical Associations (ICCA) suggested a global matchmaking platform to help build capacity in developing countries. Both of these ideas are in the current consolidated text under negotiation. Among the many outstanding issues in these negotiations, there are calls for scaling up support under each component of the integrated approach and finding innovative ways to increase finance for chemicals and wastes.

Dedicated external finance has increased, which provides some hope for the future. Unlocking private finance has proved difficult in biodiversity and climate governance too, and it remains so for chemicals and wastes management. But there are policy lessons on some price mechanisms that can be effective. Adequate attention for chemicals and wastes management is another reason to heed calls for MDB reform as part of a broader environmental mainstreaming effort. Learning lessons from the glimpses of success could help spur momentum for future financial support commensurate with the significant need to protect human health and the environment.

* * *

This document has been developed within the framework of the Global Environment Facility (GEF) project ID: 9771 on Global Best Practices on Emerging Chemical Policy Issues of Concern under the Strategic Approach to International Chemicals Management (SAICM). This project is funded by the GEF, implemented by UNEP, and executed by the SAICM Secretariat. The International Institute for Sustainable Development acknowledges the financial contribution of the GEF to the development of this policy brief.

This Policy Brief is the fourth in a series featuring cross-cutting topics relating to the sound management of chemicals and wastes. It was written by Jen Allan, Earth Negotiations Bulletin (ENB) Strategic Advisor. The series editor is Elena Kosolapova, Senior Policy Advisor, Tracking Progress Program, IISD.